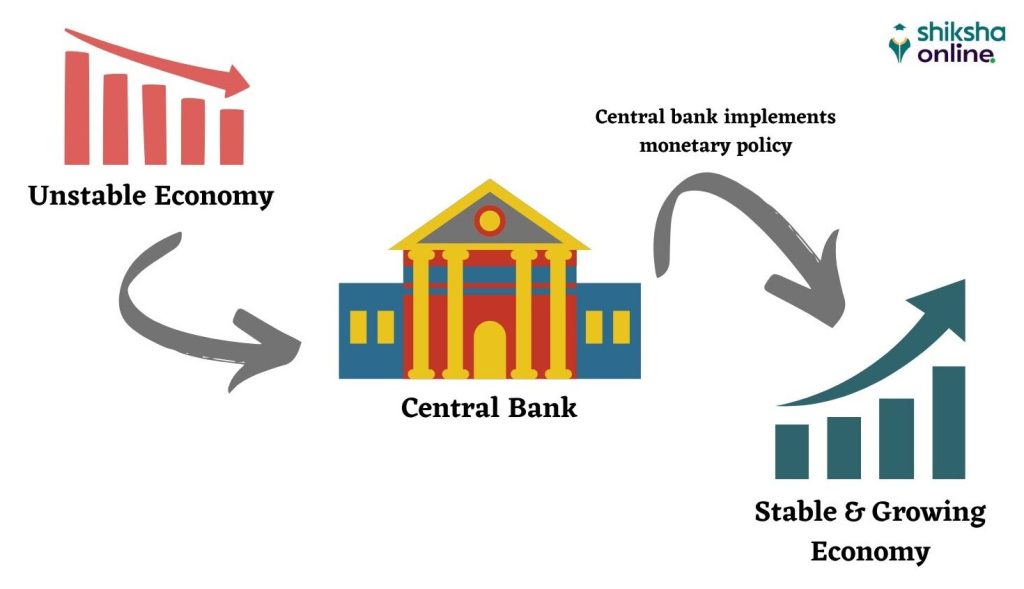

Introduction: The Crucial Role of Central Banks in Financial Stability

In an interconnected global economy, central banks play an essential role in ensuring the stability of financial markets. As the guardians of monetary policy, central banks are tasked with maintaining economic balance, preventing systemic risks, and fostering trust in the financial system. The 2008 global financial crisis highlighted the importance of central banks in managing not just domestic monetary policy but also in providing liquidity during times of global financial turmoil.

This article will explore the evolving role of central banks in financial stability, the tools they use to mitigate risks, and the challenges they face in safeguarding both domestic and international economic health.

Section 1: The Traditional Role of Central Banks

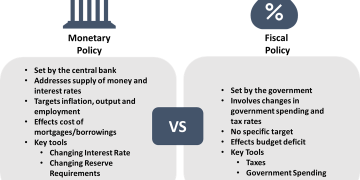

Historically, central banks were primarily responsible for regulating the money supply and maintaining price stability. Over time, however, their roles have expanded significantly, especially in response to financial crises. The initial objective of central banks was to manage inflation and ensure the value of currency remained stable. This is done by controlling the money supply through interest rate adjustments and open market operations, among other tools.

Price Stability and Inflation Control

The primary function of most central banks is to maintain low and stable inflation, typically targeting a rate around 2%. This target is designed to maintain the purchasing power of the currency while avoiding deflationary spirals or runaway inflation. To achieve this goal, central banks adjust interest rates, engage in open market operations, and influence banking regulations to control the flow of money in the economy.

However, price stability alone is not sufficient to ensure the long-term stability of financial systems. While central banks play a crucial role in controlling inflation, they also need to consider broader economic factors such as employment, investment, and productivity growth.

Lender of Last Resort

The role of central banks as “lender of last resort” is a critical aspect of their function in ensuring financial stability. During times of economic distress, such as during banking panics or liquidity crises, central banks step in to provide short-term loans to solvent but illiquid financial institutions. This emergency liquidity support prevents the collapse of banks, which could have devastating ripple effects on the broader economy.

The 2008 financial crisis saw central banks across the world adopt extraordinary measures, including the rapid extension of credit to troubled financial institutions. Central banks, including the Federal Reserve, the European Central Bank (ECB), and the Bank of England, responded to the crisis by creating emergency lending facilities, backstopping the financial system, and even purchasing distressed assets to restore market confidence.

Section 2: The Expansion of Central Banks’ Role in Financial Stability

As global financial markets have become more integrated, the role of central banks in ensuring financial stability has grown far beyond simple inflation control. In today’s complex and interconnected financial system, central banks must address systemic risks, ensure financial market liquidity, and manage a range of potential threats to global financial stability.

Systemic Risk and Macroprudential Policy

In recent years, central banks have adopted a macroprudential approach to financial stability. This involves managing risks that affect the entire financial system rather than just individual institutions. Systemic risk refers to the possibility that the failure of one large institution or market shock could trigger widespread financial instability.

The 2008 financial crisis exposed the dangers of a fragmented regulatory framework and the failure to address systemic risks in the banking and financial systems. In response, central banks have expanded their focus from microprudential regulation (focused on individual financial institutions) to macroprudential oversight, which looks at the broader health of the financial system.

This approach includes regulating large institutions whose failure could disrupt the entire system, managing credit bubbles, monitoring interconnections between financial markets, and assessing risks related to emerging markets or sectors. Many central banks now conduct stress tests on banks to assess their resilience to economic shocks.

The Role of Central Banks in Global Financial Crises

Central banks have become the first line of defense in managing financial crises. During the 2008 crisis, for example, central banks played an instrumental role in restoring financial stability by intervening in financial markets, guaranteeing bank deposits, and facilitating large-scale bailouts for struggling financial institutions.

Central banks also implemented unconventional monetary policies, such as quantitative easing (QE), which involved buying government bonds and other assets to inject liquidity into the economy. These actions were crucial in stabilizing global markets and restoring investor confidence. However, the long-term effects of these policies remain a subject of debate.

During the COVID-19 pandemic, central banks once again played a pivotal role. The Federal Reserve and other central banks rapidly lowered interest rates and provided substantial liquidity support to financial markets. In addition, central banks expanded their balance sheets, purchasing a wide range of financial assets, including corporate bonds and municipal debt, to stabilize financial markets and support economic recovery.

Section 3: The Tools of Central Banks in Maintaining Financial Stability

Central banks use a range of tools to maintain financial stability, many of which go beyond traditional monetary policy. These tools include emergency liquidity facilities, stress testing, and regulatory measures designed to safeguard the stability of the banking system.

Emergency Liquidity Support and Crisis Management

The most significant tool central banks have at their disposal in times of financial crisis is emergency liquidity support. During periods of financial instability, central banks can provide emergency loans to financial institutions to prevent insolvencies and ensure the continued functioning of the financial system. This role as “lender of last resort” is crucial to maintaining confidence in the banking system and preventing panic.

During the 2008 crisis, central banks around the world opened emergency liquidity facilities to provide short-term loans to banks facing liquidity shortages. Similarly, during the early stages of the COVID-19 pandemic, central banks rolled out massive lending programs to support businesses and individuals.

Stress Testing and Systemic Risk Monitoring

In addition to providing emergency support, central banks conduct stress tests to assess the resilience of financial institutions under adverse economic conditions. Stress tests simulate economic shocks, such as sharp declines in stock prices or rising interest rates, to evaluate how well banks can withstand financial pressure.

Stress testing helps central banks identify vulnerabilities in the financial system and take preventive measures to mitigate risks. These tests are also useful for determining whether banks have sufficient capital reserves to absorb losses during a crisis.

The Financial Stability Board (FSB) and the Bank for International Settlements (BIS) have also developed frameworks for monitoring systemic risk and ensuring that global financial institutions are adequately regulated.

Regulatory Measures and Macroprudential Oversight

In recent years, central banks have placed more emphasis on macroprudential regulation to prevent excessive risk-taking and ensure the stability of the financial system. These measures include setting capital requirements for financial institutions, regulating lending standards, and limiting speculative activity in asset markets.

For example, central banks may require banks to hold higher levels of capital during periods of economic growth to buffer against potential losses in the event of a downturn. They may also implement “counter-cyclical” measures, such as increasing capital buffers during periods of strong growth, to reduce the risk of an economic bubble.

Section 4: Challenges to Global Financial Stability

Despite the best efforts of central banks, there are several challenges to maintaining global financial stability. These challenges include the increasing complexity of financial markets, the rapid pace of technological change, and the interconnectedness of global economies.

Global Interdependence and Financial Contagion

In today’s globalized economy, financial markets are highly interconnected. A crisis in one country can quickly spread to others, as seen during the 2008 global financial crisis. The interdependence of global financial institutions means that a disruption in one part of the financial system can trigger a cascading effect that impacts economies worldwide.

Central banks must therefore coordinate their policies and responses to ensure that they manage financial contagion effectively. The role of the G20, the Financial Stability Board (FSB), and the International Monetary Fund (IMF) has become increasingly important in fostering international cooperation in managing global financial stability.

Technological Risks and the Rise of Cryptocurrencies

The rise of digital currencies and fintech innovation poses new risks to global financial stability. Cryptocurrencies like Bitcoin and Ethereum, as well as decentralized financial systems (DeFi), challenge traditional financial regulatory frameworks. The lack of regulation around digital assets presents new risks related to market volatility, money laundering, and financial fraud.

Central banks are grappling with how to regulate and integrate digital currencies into the existing financial system. The European Central Bank and the People’s Bank of China have explored the creation of central bank digital currencies (CBDCs), which could offer greater control over digital assets while ensuring financial stability.

The Challenge of Climate Change

As global economic risks evolve, climate change has emerged as a significant factor affecting financial stability. Extreme weather events, such as floods, hurricanes, and wildfires, can disrupt economies and damage infrastructure, leading to significant financial losses.

Central banks are increasingly integrating climate-related financial risks into their stability frameworks. The Bank of England and the European Central Bank are already assessing the potential impact of climate change on financial markets and are considering ways to address the risks associated with the transition to a low-carbon economy.

Conclusion: The Future of Central Banks in Maintaining Global Financial Stability

As the world’s financial systems continue to evolve, central banks will play an increasingly important role in maintaining financial stability. The tools and strategies they employ must be flexible and responsive to both traditional risks and emerging challenges, such as technological innovation and climate change.

Central banks must continue to adapt to new threats and coordinate with international financial institutions to ensure the global financial system remains resilient in the face of future crises. Their role as lenders of last resort, systemic risk monitors, and economic stabilizers will continue to be crucial in shaping the future of global financial stability.

{kind=link}